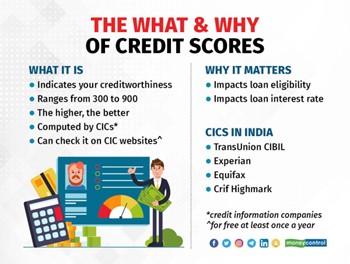

If you are planning to take a loan, one of the first things a lender will check is your credit score. It plays an important role in a bank’s decision on approving a loan. In fact, credit scores can also influence the interest rates offered to you.

Put simply, a credit score is an indicator of your creditworthiness. Credit information companies (CICs) such as Experian, TransUnion CIBIL, Experian, Equifax and Crif Highmark provide credit scores based on your credit history data. The score can range anywhere from 300 to 900 – the higher the score, the better it is. It provides a lender with some comfort on your creditworthiness or the likelihood of you re-paying the loan.

All CICs in India allow you to check your credit score for free at least once a year.

So, what are the factors that can impact your credit score?

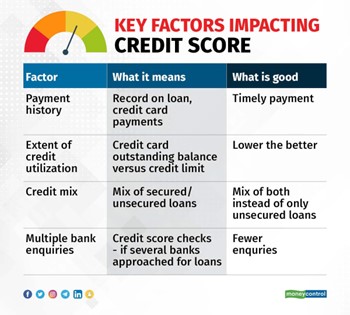

Repayment track record, credit utilisation limit

Highlighting repayment history as one of the most important factors that impact your credit score, Saikrishnan Srinivasan, MD, Experian Credit Information Company of India, says, “Timely payment of loans and credit card bills positively impact your credit score, while late or missed payments can reduce your credit score significantly.”

Another important factor is your credit mix. “Having a well-managed combination of secured and unsecured loan accounts can help you maintain a healthy credit score,” says Srinivasan. Manish Ajwani, a former Product Head and Assistant Vice President at TransUnion CIBIL, explains this. For example, having only unsecured credit (not backed by collateral) such as a personal loan and credit card instead of say, a mix of a home loan (secured loan) and a personal loan (unsecured loan) may impact your credit score, he says.

Credit utilisation, or the percentage of your credit limit that you are utilising, also has a role to play in your credit score. Ajwani says the closer your credit card outstanding balances are to the credit limit, the higher impact it has on your credit score since the lender views this as an indicator of high risk. So it helps to keep the credit utilisation low.

The length of your credit history also plays a vital role in your credit score according to Srinivasan. For example, if you have a home loan that you have been regularly servicing for say the last 8-10 years, then that can have a positive impact on your credit score.

Lower scores for credit hungry borrowers

Your credit score can also get adversely impacted if you have contacted many banks for a loan. “When a bank or lender checks your credit score during a loan or credit application, it may have a temporary impact on your credit score. Multiple inquiries within a short period can be concerning and potentially lower your credit score,” says Srinivasan.

But remember, this is not applicable to your own regular monitoring of your credit score. It may, in fact, be a good idea to check your credit score periodically to ensure there are no discrepancies. If there are any, you can contact the CIC to get these rectified.

CICs are covered under RBIs’ Integrated Ombudsman Scheme. So if you have a grievance against any CIC, you can file a complaint with the Ombudsman. This can be done in multiple ways – online complaint filing on the RBI website, sending an email, sending the complaint form by post, or by calling the contact centre over the phone.

Furthermore, in the April 2023 monetary policy meeting, the RBI governor announced that given the increase in consumer complaints against CICs, a comprehensive framework would be set up for grievance redressal and customer service by CICs. Among the measures announced was a proposal to put in place a compensation mechanism for delayed rectification of credit information. The CICs will also have to specify the timeframe within which data received from lenders will get updated in their databases. Once these proposals take effect, the rectification of errors in credit scores or credit reports is expected to get easier.